If you sit on a condominium board or manage a community, major shifts are changing how lenders approve conventional mortgages for your units. On March 18, 2026, Fannie Mae and Freddie Mac announced coordinated updates tightening condominium project eligibility standards.

The core focus of these changes? Reserves Studies and Funding.

These rules aim to promote better long-term financial health for communities. And reduce risks from underfunded reserves (like sudden special assessments or deferred maintenance). If your association doesn’t adapt, buyers may lose access to conventional financing, which can directly hurt property values.

Here is a breakdown of what is changing, when it happens, and how a professional reserve study keeps your community compliant.

-

The Big Shift: Reserve Funding Minimum Goes to 15%

Under the standard “Full Review” process, lenders look directly at an association’s budget.

- The New Rule: Condo associations must now allocate at least 15% (up from 10%) of their total annual budgeted assessment income to replacement reserves.

- Effective Date: This becomes mandatory for loan applications dated on or after January 4, 2027 (though lenders are encouraged to implement it earlier).

Tip: If your association cannot or does not want to automatically dedicate 15% of its budget to reserves, you can still qualify if you rely on a qualifying, up-to-date professional reserve study.

-

Strict New Rules for Reserve Studies

Using a reserve study to justify your budget flexibility comes with much stricter parameters under the new guidelines:

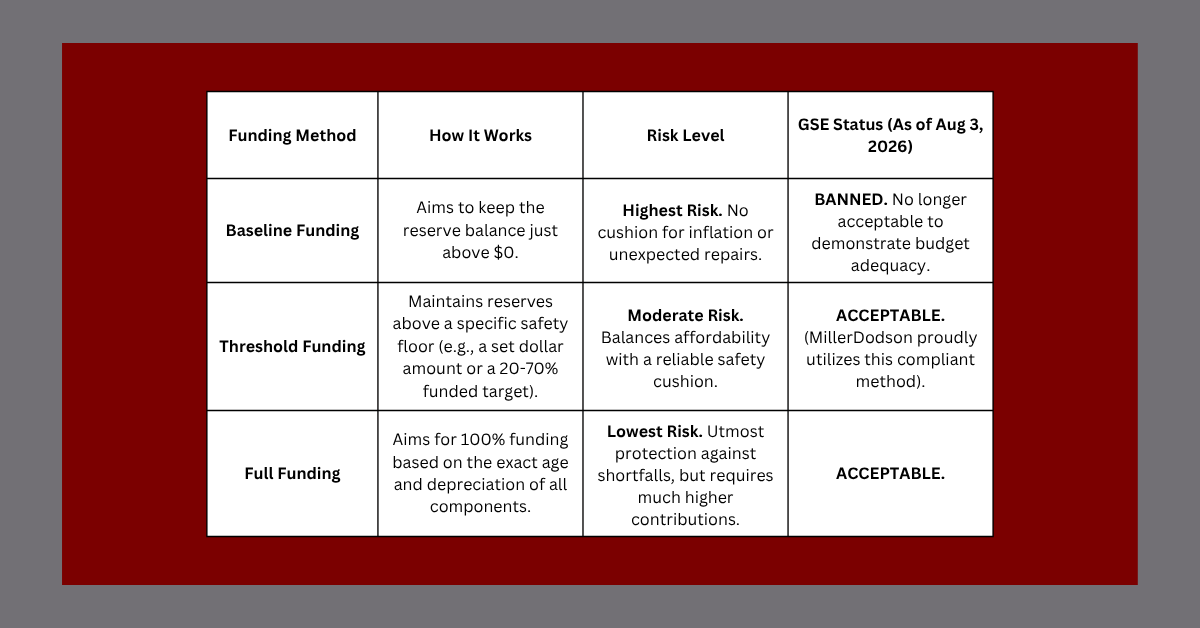

- No More “Baseline” Funding: Studies using the baseline funding method (aiming to keep the cash balance just above zero) are no longer permitted by lenders.

- The “Highest Recommendation” Rule: If you use a reserve study to override the 15% rule, your association’s budget must follow the highest recommended reserve allocation outlined in that study.

- The 3-Year Expiration Date: The reserve study (or formal update) must be no more than 36 months (3 years) old at the time of the lender’s project review.

- Independent Experts Only: The study must be prepared by an independent third party with specific expertise. It must also feature a full component inventory, a financial analysis of current adequacy, and a compliant funding plan.

- Effective Date: These reserve study enhancements are mandatory for loan applications dated on or after August 3, 2026.

-

The Retirement of “Limited Reviews”

To make things more urgent, Fannie Mae and Freddie Mac are retiring the “Limited Review” (or streamlined review) process for most established condo projects on August 3, 2026.

This change forces almost all established communities into a Full Review. Consequently, lenders will aggressively audit your finances, reserve balances, and reserve studies.

Understanding the Funding Methods: Why It Matters

When you get a reserve study, it typically maps out expenses over 30 years using a cash flow method. Lenders are now looking very closely at the funding goal used in your study:

Because Threshold Funding represents a mathematically sound, safe option that avoids the high costs of Full Funding while steering clear of the now-banned Baseline method. It serves as an excellent pathway to compliance for most associations.

How to Protect Your Community

To keep your condo units marketable and ensure buyers can secure conventional mortgages, your board should act immediately:

- Review your current budget allocation against the upcoming 15% mandate.

- Check the date on your last reserve study—if it’s nearing or past the 3-year mark, it needs an update.

- Ensure your study relies on an approved Threshold or Full Funding model.

For the exact policy wording, you can view the official announcements here:

- Read the Fannie Mae Lender Letter LL-2026-03 and Selling Guide.

- Read the Freddie Mac Bulletin 2026-C and Seller/Servicer Guide.

Ensure Your Community Stays Compliant

Don’t let outdated financials or an expired study halt home sales in your community. We specialize in providing fully compliant, independent reserve studies using approved Threshold Funding methods to keep your association stable and eligible.

Ready to protect your property values? Click here to request a reserve study proposal for your association.